I share with probably a majority of voters the opinion that Malcolm Turnbull would do a better job of leading Australia than any other realistic candidate.

I don’t agree with everything Malcolm says or does, but then who would? Right now he is constrained by “cabinet solidarity”. That farcical party political convention that forces him to say and do things that his body language and his choices of expression says he doesn’t really believe. Freed of that constraint, I suspect that we would all find Malcolm an even more positive force for the good of Australia.

When we were going through that nonsense after the August 2010 election of piecing together a new Government I emailed Malcolm thus:

Message To Malcolm: I reckon the 100+ year old Constitution, the 100 year old Labor Party and the 60 year old Liberal Party are ALL past their use by date. In the current situation YOU have a golden opportunity to lead Australia towards a genuine new 21st century political and government paradigm (maybe a republic?). Why not go to the cross benches, get a dozen or more of the smartest MPs to follow (hardly a challenge I would have thought). Then demand that you be PM leading a real Government! … What’s your alternative? … 3 years in the opposition? …. What a waste …. SEIZE THE MOMENT … regards … Geoff O’Reilly

Somewhat to my surprise, I found myself put on Malcolm’s social media database, and received the following reply on 1st September 2010:

Dear Geoff,

Thank you for writing – I appreciate your support. However I am committed to the Coalition, and look forward to being a part of a new Coalition Government.

Best wishes, Malcolm

I guess at that time Malcolm was fondly hoping there would in fact be a new Coalition Government. But it was not to be. On the 7th September Windsor and Oakshott chose to support Labor. So I rather cheekily sent Malcolm this:

Well then … you blew that opportunity, didn’t you … where to now? … get out of the 9 dots box … why not ask Julia for a cabinet position and make a serious contribution to the nation’s good government, maybe?

This time he didn’t respond … or take my advice! What a pity …

In opposition, Malcolm patiently turned the then Liberal policy to completely dismantle the NBN into a policy that meant we would at least have an NBN backbone, and he cunningly left the door wide open for it to be turned into the real thing over time. The NBN is a vital piece of infrastructure for Australia’s long term future. Malcolm knows that. He also knows that taking Abbott full on, head on over the NBN would get him nowhere. So he’s outsmarted Abbott and we have the NBN policy we have. Good politics!

Now in Government he seems to be very quietly and successfully getting on with the job of giving us the “NBN we can have” – for now. Tomorrow is another day, and no options are off the table.

Then, in all the furore pre- and post- the Budget, Malcolm has kept a very low public profile, notwithstanding his eminent qualifications to be an important and highly credible messenger to the Australian public of what we really need to be focused on for our own good. Instead we have had to listen to the blatherings of ministers like Pyne, Dutton, Cormann, Abetz and Andrews as support acts to Abbott and Hockey.

Why?

I reckon there will be two reasons:

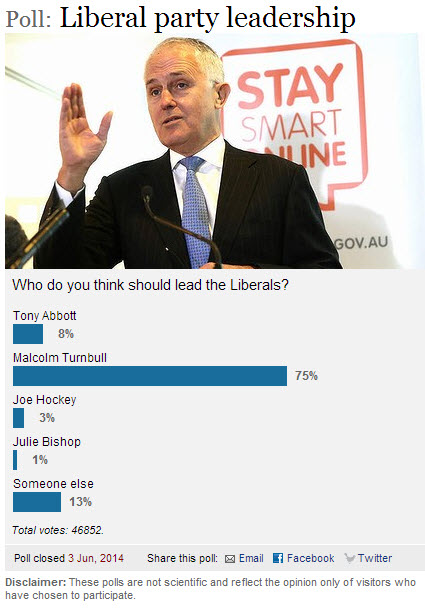

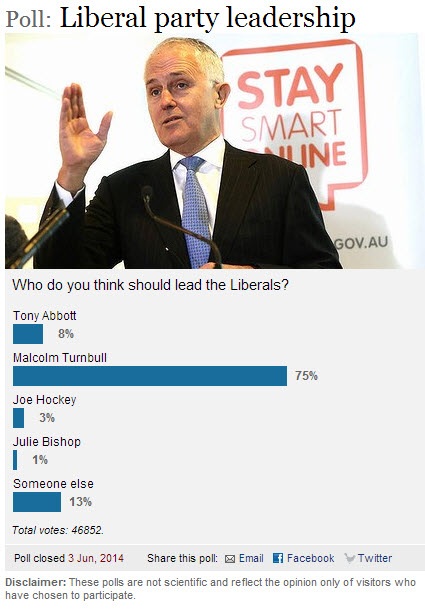

- Malcolm is just too good, too popular and too credible for Abbott to let him loose. That would be bad for Abbott. In support of this idea, look at this SMH poll that closed just three days ago with almost 47,000 responses:

- Malcolm struggles with the Abbott philosophy. (Of course, he would, in the name of government solidarity, deny that. Just as, in the last few days, he has repeatedly “supported the government” and told us how united it is.) Hmmmm …

Let’s follow this second idea for a minute and see what we might get as a “set free” Turnbull philosophy.

First, the squawking extreme right commentariat (Bolt, Jones, the Australian and others) would struggle for a look in. Politicians like Brandis, Bernardi and others like them would be ever so politely be ignored. And, where necessary all of the forgoing would be taken on with calm reasoned debate about ideas, not retaliatory squawking. Just look for evidence at the events of this week over the “Palmer dinnergate”, and Malcolm’s willingness and ability to get stuck in to Bolt and Jones afterwards.

Second, the recent budget attack on those less fortunate and less able to look after themselves would be reversed. This week I had an email from Malcolm (along with thousands of others I guess). It started thus:

“Geoff, I’ll be Sleeping Out for St Vinnies

The mark of a great society is the way it treats the neediest and most vulnerable …”

So how do you think Malcolm really thinks about the Abbott philosophy embedded in the Budget?

Third, I think Malcolm would espouse a conservative fiscal approach. He would certainly cut into unnecessary expenditure and welfare (and there’s plenty of that), but it would be accompanied by a preparedness to take on the debates about where the money has to come from (genuine tax reform would be front and centre of the agenda). Wise men like Ken Henry would be listened to. He would create understanding that some debt, for financing long term assets of the nation, is smart: but debt to fund recurrent expenditure is not sustainable. And so on.

Fourth, Malcolm’s clear discomfort with our current immigration/asylum seeker policies would see us adopt a manifestly more humane policy, rather than the misguided populist stance we now have.

Fifth, he would make a peerless ambassador to the world. No more embarrassing nonsense: (like that recently with Indonesia). We would expect (and get) smart navigation of the delicacies of things like the relationships with China and Japan: both so critical to our economy and trade, but currently squabbling over rocks (and oil reserves?) in the South China Sea. We would no longer be the unquestioning Deputy Sheriff for the US in Asia.

We would price carbon and respect the environment. Malcolm’s credentials and beliefs in this regard are long standing and unquestioned.

We would get a good NBN soon … and a better one later.

He would advocate a vision, for the long term, for sustainability, for fairness …

But I wax on …

You get the idea. Why doesn’t Malcolm be Malcolm in the Middle. Toss away the loony right wing neo-con zealots. Avoid being beholden to the far left, to Unions … to any pressure groups for that matter.

Lets make a fresh start. Stand up and lead the middle, Malcolm. You might be surprised how many smart people (from both side of the current political fence) would follow.

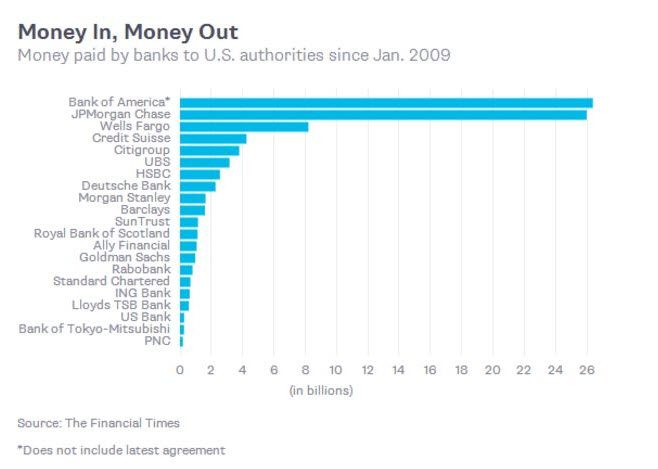

This adds up to about US$87.5 billion.

This adds up to about US$87.5 billion.