No-one seems to understand why, but this time of year is often tumultuous. (Particularly in the financial world. 1929. 1987. 2008.) This year is looking pretty interesting too.

So called “geo-political risk” has risen sharply.

Gaza and Ukraine have settled down for now. Lots of fighting, MH17 shot down, many deaths, lots of destruction, but nothing resolved. These trouble spots will surely flare again, because if you go to the root causes (who should live where in the Jordan Valley, and NATO’s relentless advance to Russia’s doorstep), nothing’s changed.

Attention has now turned to Iraq and Syria. Looks to me like the current tactics and behaviour of the West has about zero chance of resolving anything, and a good chance of making things a lot worse. The IS warriors look to be a nasty bunch, but really no worse than an endless list of ugly groups and regimes. (Who remembers Pol Pot or Idi Amin, just for example?). Bombs will not resolve centuries old enmities, or productively occupy idle young men.

In Hong Kong, the predominantly young (… it’s always the young ones!) have come out bravely and in large numbers to protest for what appears to be a quite small step in their governance. Despite the current lull, a long, on-going, serious challenge for the mandarins in Beijing lies ahead: how to govern a youthful, educated, connected, and rising Chinese middle class?

The list of failed states seems to increase by the month. Libya. Next a few in west Africa?

And, the ebola virus has now escaped west Africa to the US and Europe. Back in Sierra Leone, 121 died in one day this week. This could get really nasty.

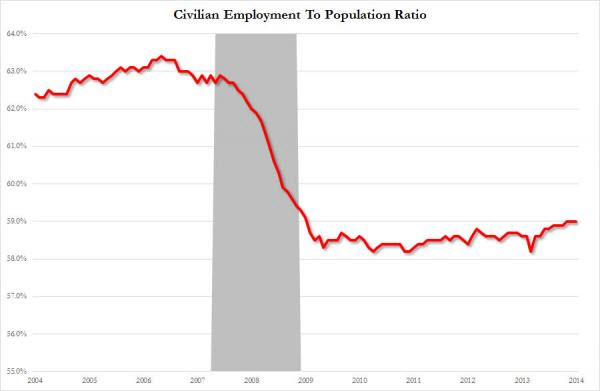

Economic performance has turned down just about everywhere …

President Obama is out on the stump for the mid-term elections coming next month, arguing that US economy is recovering. He’s quoting all sorts of numbers about new jobs, and crowing because unemployment has dropped below 6%.

Poor guy, he’s tried really hard, but it’s a delusion.

We all know that economies must under-perform if households don’t/can’t spend. US households are still up their necks in debt (student loans, car loans, mortgages, credit cards). The US Bureau of Census has just announced that real household income has now fallen back to where it was 20 years ago. And the percentage of the population in the US workforce is not even close to recovering the ground lost in 2008 …

In Europe, the motor is sputtering just at the time when things should be getting to work. All the major economies, Germany, France and Italy are in recession, or all but. Germany is the manufacturing heartland, but factory orders in August fell 5.7% … oops.

Over in Japan things are going from bad to worse. Abenomics has failed. The economy is going backward again, and fast: down 7% in the second quarter and probably barely positive in the third quarter just finished.

It’s always hard to work out what’s really going on in China, but except for the odd spot of (probably made up) positive news, it’s all looks bad. China’s recent growth has been built on a massive bubble of debt used to finance infrastructure and housing. Now the housing bubble is deflating. The iron ore price has tanked. Worse is coming.

Australia is muddling along. But the miners are taking a battering, the Government is squeezing and unemployment rising.

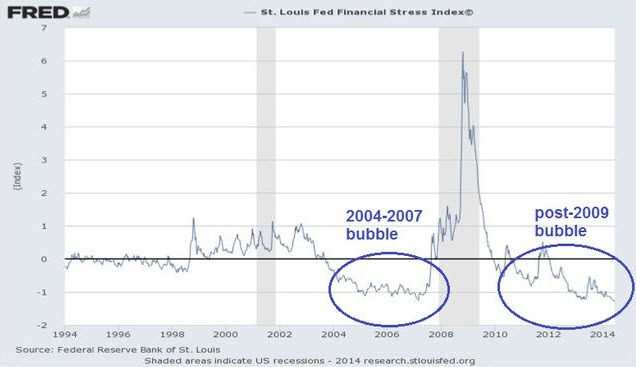

… but the party is rolling on in the financial markets … or is it?

Wall Street has retreated a little from it’s top, but is still very high by any standard. It has been propelled by freshly printed money (about $3.5 trillion); huge buybacks of shares (dividends and share buybacks have recently been consuming more than 90% of corporate cash – so not much productive investment going on there); and frothy valuations of tech related stocks. One of my favourites is the Facebook purchase of Whats App at $22 billion. Whats App has 500 million subscribers, no advertising, and just the potential to earn $1 per subscriber per year. Value 44+ times revenue? … Hmmm, not sure about that!

October will be interesting …

…and if you got the time check this out