House prices remain very topical right around Australia. Here in my country town, extra activity is certainly generating greater stability in prices, and even in some sub-areas prices have risen just a bit. This is regional Australia. How different to the big cities!

In the great conurbations of Sydney and Melbourne, where about half Australians live and most of the jobs are, the heat is on, albeit there is some sign now of the temperature easing a bit from the height of last summer’s excitement.

Commentators are mostly trying to have a bit each way: not sure if they want to assure listeners/readers that everything is OK, or warn them of potential downside. Above all they want to be able to say, I told you so …

Today the Sydney Morning Herald took an unusual stance (for them) with this headline:

Housing bubble fears: property prices could fall 10 to 20 per cent

The commentator went on with this:

The $4 trillion Australian housing market is now overvalued by at least 10 per cent. Every day, valuations get more stretched. Indeed, Australia is just months away from having the most expensive residential property market in history.

Anyone with exposure to the banks, which account for one-third of the sharemarket’s value, or to housing, should be focused on two questions.

When will a bona fide bubble emerge and how steep are the price falls likely to be when borrowing costs are normalised?

… and concluded with this:

When prices do start sliding, it is not inconceivable that we could see unprecedented 10 to 20 per cent losses across the board.

This has ramifications for home owners and investors in the banks, which are, on average, leveraged 25 times and only need a circa 5 per cent fall in the value of the assets held on their balance sheets – 60 per cent of which are home loans – to have their equity capital wiped out. My message is: buyers beware.

The Governor of the Reserve Bank continues to tell banks to be cautious with mortgage lending and hinting that constraints may need to be directed very specifically on lending for housing. This has already been done in NewZealand, Singapore and Hong Kong, countries with “hot” property markets.

I think a move soon towards such policy in Australia is inevitable. The RBA is otherwise stuck with a need to raise interest rates to cool the housing market, whilst at the same time needing to lower them to knock down the Australian dollar and stimulate the productive real economy. A classic dilemma.

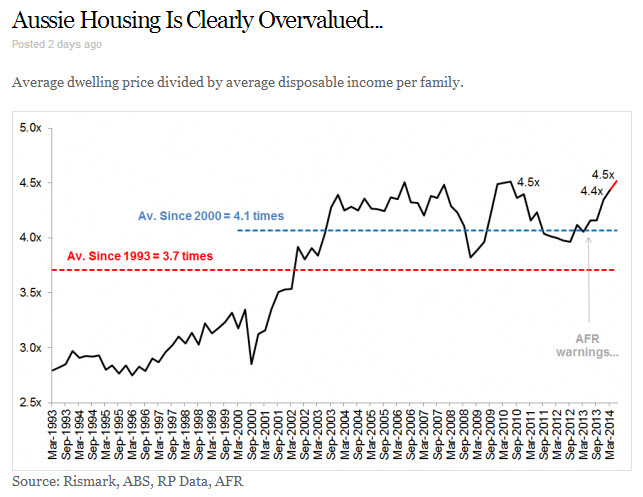

And well might the RBA be concerned. The graph below that has appeared in a few places in the last week shows that Australian housing affordability is currently at its all-time worst, and getting worse. At 4.5 times family disposable income, we are now in an era where two incomes are mandatory to afford a house.

Not only is this an economic and financial issue, it is very directly a social issue. It creates things like the intense pressure on child day care; pressure on rental housing and social housing.

Not only is this an economic and financial issue, it is very directly a social issue. It creates things like the intense pressure on child day care; pressure on rental housing and social housing.

Governments everywhere are stuck, and out of ideas. The problems materialize in different ways in different countries, but there is a theme, housing the population in an acceptable affordable manner requires big tough policy choices. And, not many politicians are up to the job.

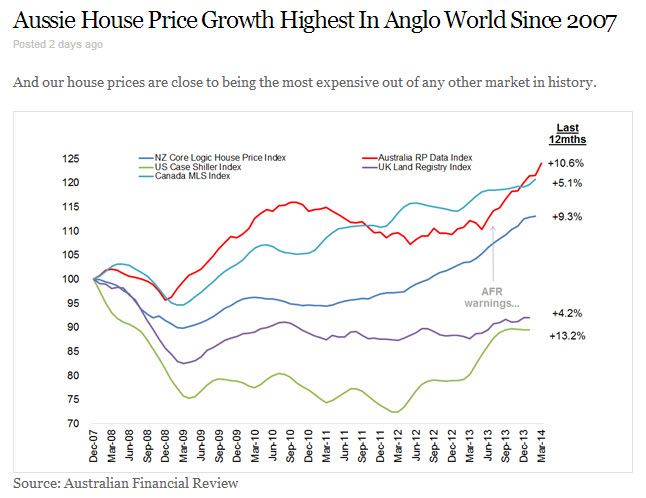

Here’s another perspective on house prices. This graph above is a comparison of the movement in house prices since 2007 in the “anglo world”. Australia (red line) and Canada (light blue line) have shot ahead. (Like Australia, Canada has a huge resources sector.) New Zealand has too, and they are now acting directly to try to cool things down. The UK (purple) and the US (green) are still down from 2007.

Whilst many are reluctant to call Australian house prices a bubble, there is no doubt they are precariously high, riding on huge credit facilities from the big four banks. So, as the real economy continues to weaken, soft incomes will simply force prices to down.

So I’m “looking out below” … When will the turning come? … Anyone’s guess, but pretty soon, I reckon.